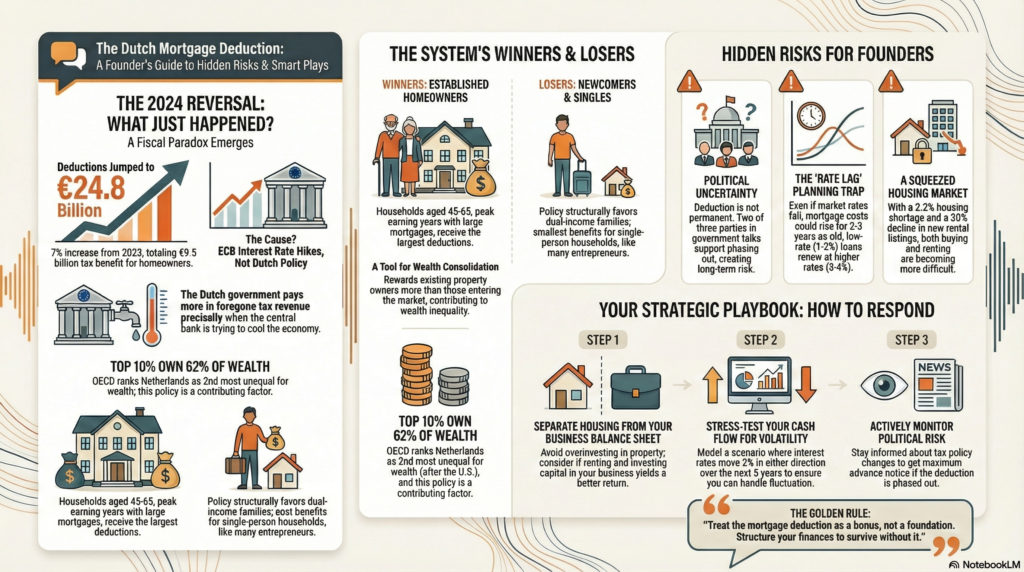

Dutch mortgage tax deductions rose 7% in 2024 to €24.8 billion after years of decline. ECB interest rate increases drove the reversal, not policy changes. This creates fiscal volatility for entrepreneurs and exposes how the system favors existing homeowners over market entrants.

Core Facts:

- Dutch homeowners deducted €24.8 billion in 2024, up 7% from 2023, with total tax benefits reaching €9.5 billion

- Rising ECB interest rates increased mortgage costs, which increased tax deductions despite cooling monetary policy

- Households aged 45-65 receive the largest deductions while single-person households get the smallest benefits

- Two of three parties in government formation talks support phasing out the mortgage tax relief system

- Many fixed-rate mortgages locked at 1-2% are now renewing at 3-4%, creating a lag effect in cost reductions

LISTEN TO THE DEEP DIVE ABOUT THIS TOPIC:

Why the Dutch Mortgage Deduction Reversed in 2024

I’ve been watching Dutch mortgage tax deductions for years. The trend was predictable: steady decline, year after year. Then 2024 happened.

Dutch homeowners deducted €24.8 billion from their taxable income in 2024. That’s up 7% from 2023. The total tax benefit hit €9.5 billion.

This is the second annual rise in a row after years of decline.

The mechanism behind the reversal matters more than the number.

What Triggered the 2024 Reversal

The European Central Bank raised interest rates. Dutch mortgage holders with variable rates or those refinancing faced higher monthly costs. Higher interest payments mean larger tax deductions.

This creates a fiscal paradox. When the ECB tightens monetary policy to control inflation, it increases the Dutch government’s implicit subsidy to homeowners. The government pays more in foregone tax revenue precisely when trying to cool the economy.

For micro and small entrepreneurs, this exposes a structural risk. You plan your business finances assuming stable housing costs. Your mortgage deduction benefit now moves with ECB decisions you don’t control. That’s rate volatility translating directly into fiscal exposure.

Bottom line: ECB monetary policy now drives Dutch fiscal policy outcomes through mortgage deductions, creating unpredictable cash flow impacts for entrepreneurs.

Who Benefits From the Dutch Mortgage Deduction

I looked at who benefits from this system. The pattern is clear.

By age group:

- Households aged 45-65 receive the largest absolute deductions

- They’re in peak earning years, carrying substantial mortgage debt on properties bought when prices were lower

- Households over 65 have smaller deductions because they’ve paid down mortgages

- They’ve already captured decades of tax benefits and property appreciation

By household type:

- Single-person households get the smallest benefits

- The policy structurally favors family units with dual incomes and larger properties

- Single entrepreneurs face higher prices driven partly by tax incentives they benefit from less

The OECD ranks the Netherlands as the second most unequal country in terms of wealth after the U.S., with the top 10% owning 62% of total wealth (excluding pensions).

The mortgage deduction doesn’t create this inequality alone. But it functions as an intergenerational wealth consolidation tool that makes it harder for new entrants to build equity.

Key insight: The system rewards people who already own property more than it helps people trying to enter the market.

What Are the Political Risks to the Mortgage Deduction

Two of the three parties in Dutch government formation talks have backed calls to phase out the mortgage tax relief system.

The Netherlands also agreed to reduce mortgage tax relief to around 37% as part of the EU’s coronavirus recovery plan. Brussels still owes €4 billion under that agreement.

This creates decision uncertainty for entrepreneurs planning property investments. If you’re buying commercial property or a home to secure your business operations, you’re making a 20-30 year decision based on tax rules that might fundamentally change within 5 years.

Research from ABN Amro found that a large proportion of Dutch homeowners wouldn’t struggle financially if the deduction were reduced or abolished. The policy is more about wealth accumulation than affordability support.

That finding weakens the political defense of the current system.

Reality check: Tax policy you plan around today might not exist in 5 years. Build flexibility into your property decisions.

How the Mortgage Rate Lag Effect Distorts Financial Planning

The ECB cut rates eight times from June 2024 to June 2025. The deposit rate reached 2.0% by December 2025.

You’d expect mortgage costs to fall. Here’s the mechanism most people miss.

Many fixed-rate mortgages issued during low-interest periods are still repricing at higher rates. New mortgages get cheaper rates. Existing mortgages locked in at 1-2% are now renewing at 3-4%.

The average interest rate paid by households continues to increase even as new lending rates fall.

This creates a paradox for financial planning. Market signals tell you rates are dropping. Your costs might still be rising for another 2-3 years depending on when you locked your rate.

Planning trap: Don’t assume falling market rates mean your mortgage costs will drop immediately. Check your renewal date.

How Should Entrepreneurs Respond to Mortgage Deduction Volatility

There are three control points worth installing now:

1. Separate your housing decisions from your business balance sheet

The mortgage deduction creates an incentive to overinvest in property. That ties up capital you might deploy more productively in your business.

Model both scenarios: property ownership with tax benefits versus renting and investing the difference in business growth.

2. Build rate volatility into your cash flow projections

If you’re carrying mortgage debt, assume rates could move 2% in either direction over the next 5 years. Stress test your cash position against that range.

The deduction cushions the impact, but it doesn’t eliminate it.

3. Monitor the political risk actively

Subscribe to updates on government formation and tax policy changes. If the deduction gets phased out, you want maximum advance notice to adjust your capital structure.

Don’t assume the current rules are permanent.

Action summary: Treat the mortgage deduction as a bonus, not a foundation. Structure your finances to survive without it.

What Housing Market Pressures Affect Entrepreneurs

The Netherlands faces a 2.2% housing shortage. Building permits declined for the second consecutive year, dropping to around 44,000 on a 12-month rolling basis compared to 57,000 the year before.

The 2024 Affordable Rent Act reduced the private rental market segment. Pararius reported a 20.2% decline in new listings in Q3 2024. Many private landlords sold their properties.

This creates a squeeze on both ownership and rental options.

For single entrepreneurs and those without significant capital, the path to housing security narrows. The mortgage deduction benefits people who already own property more than it helps people trying to enter the market.

The policy was designed to promote homeownership. In practice, it now protects existing homeowners while making entry harder for newcomers.

Market reality: Both buying and renting are getting harder because the mortgage deduction raises prices for new entrants while benefiting existing owners.

The Decision Framework for Property Purchases

I don’t treat the mortgage deduction as a reason to buy property. I treat it as a secondary benefit that reduces the cost of a decision I’d make anyway.

If you need the deduction to make the numbers work, you’re probably overextending.

The system rewards people who can afford property without the tax benefit. It provides less help to people who actually need affordability support.

That’s the mechanism most founders miss.

The reversal in 2024 wasn’t a policy change. It was an interest rate change that exposed how much government fiscal policy now moves with ECB decisions.

You don’t control that volatility. You structure your finances so you’re not dependent on it staying stable.

The mortgage deduction is large, visible, and politically defended. That doesn’t make it permanent.

Build your business and personal financial structure assuming it could shrink or disappear within a decade.

If it stays, you benefit. If it goes, you survive.

Frequently Asked Questions

Why did Dutch mortgage deductions increase in 2024 after years of decline?

The European Central Bank raised interest rates to control inflation. Higher interest rates mean higher mortgage payments, which create larger tax deductions. The increase is driven by monetary policy, not changes to the deduction rules themselves.

Who receives the largest mortgage tax deductions in the Netherlands?

Households aged 45-65 receive the largest absolute deductions. They typically carry substantial mortgage debt on properties bought when prices were lower. Single-person households receive the smallest benefits because the policy structurally favors dual-income family units with larger properties.

Is the Dutch mortgage deduction going to be eliminated?

Two of three parties in government formation talks support phasing out the system. The Netherlands also agreed to reduce mortgage tax relief to around 37% as part of the EU’s coronavirus recovery plan. While the deduction is politically defended, it faces significant reform pressure.

How does the mortgage rate lag effect work?

Many fixed-rate mortgages locked at 1-2% during low-interest periods are now renewing at 3-4%. This means your mortgage costs might keep rising for 2-3 years even as market rates fall, depending on when your fixed rate expires.

Should I buy property because of the mortgage deduction?

No. The deduction should be treated as a secondary benefit, not the reason to buy. If you need the deduction to make your property purchase affordable, you’re likely overextending. Structure your finances to survive without it.

How does the mortgage deduction affect wealth inequality in the Netherlands?

The deduction functions as a wealth consolidation tool. It benefits people who already own property more than people trying to enter the market. The OECD ranks the Netherlands as the second most unequal country in terms of wealth after the U.S., with the top 10% owning 62% of total wealth (excluding pensions).

What should entrepreneurs do about mortgage deduction volatility?

Separate housing decisions from your business balance sheet. Build rate volatility of plus or minus 2% into cash flow projections. Monitor political developments around tax policy changes. Don’t assume current rules are permanent.

How does ECB policy affect the Dutch government’s fiscal position through mortgages?

When the ECB raises rates to control inflation, it increases the Dutch government’s implicit subsidy to homeowners through larger tax deductions. The government pays more in foregone tax revenue precisely when trying to cool the economy, creating a fiscal paradox.

Key Takeaways

- Dutch mortgage tax deductions rose 7% in 2024 to €24.8 billion. ECB interest rate increases drove up mortgage costs and tax deductions, not policy changes.

- ECB monetary policy now drives Dutch fiscal policy outcomes through mortgage deductions. This creates unpredictable cash flow impacts for entrepreneurs who don’t control rate decisions.

- The system benefits households aged 45-65 most while single-person households get the smallest benefits. It functions as a wealth consolidation tool that favors existing homeowners over market entrants.

- Two of three parties in government formation talks support phasing out the mortgage tax relief system, creating political risk for long-term property investment decisions

- Fixed-rate mortgages locked at 1-2% are now renewing at 3-4%. This creates a lag effect where your costs might rise for 2-3 years even as market rates fall.

- Treat the mortgage deduction as a bonus, not a foundation for property purchases. If you need the deduction to make the numbers work, you’re overextending

- Build your business and personal financial structure assuming the deduction could shrink or disappear within a decade to protect against policy changes you don’t control