PSD3 compliance is due by late 2027. The regulatory burden falls on payment providers, but the operational consequences hit Dutch small businesses. The real risk is the 18 to 24 month transition period. Inconsistent provider updates will create silent payment failures, cash flow mismatches, and conversion drops. You need to map your payment dependencies, test authentication flows monthly, and read updated terms before clicking accept.

What Dutch Entrepreneurs Need to Know About PSD3

- PSD3 becomes mandatory by end of 2027. iDEAL disappears completely in 2027 as it transitions to Wero.

- Enhanced security measures add verification steps. More friction leads to higher payment abandonment rates.

- Payment providers will update systems at different speeds. This creates inconsistent authentication flows and silent transaction failures.

- Updated terms of service will shift liability for failed authentication, refund processes, and settlement timing.

- Three controls prevent expensive surprises: map provider dependencies, test checkout flows monthly, and read updated terms carefully.

LISTEN TO THE DEEP DIVE ABOUT THIS TOPIC:

What is PSD3 and When Does it Take Effect?

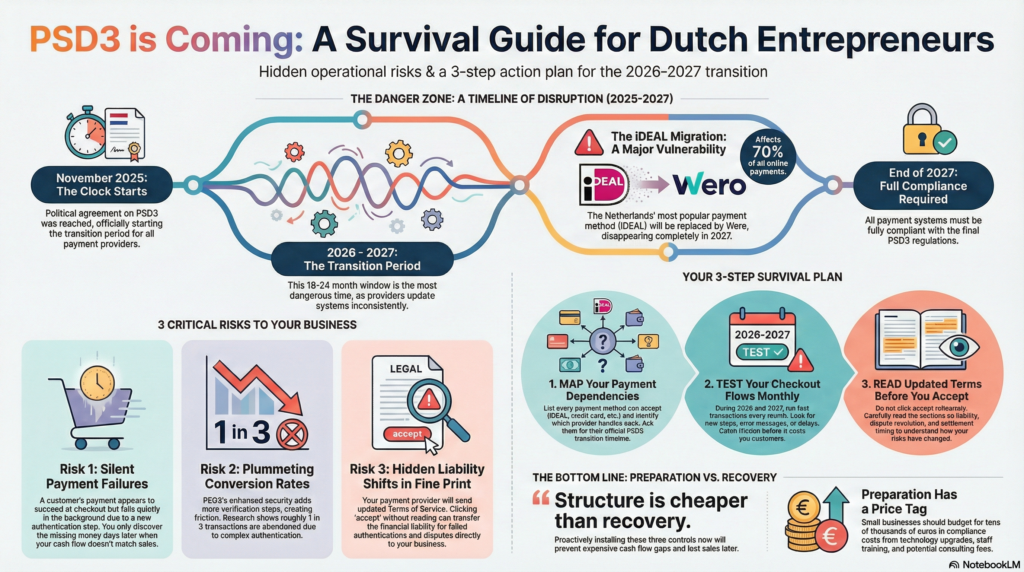

The political agreement on PSD3 and PSR was reached in November 2025. Full compliance is expected by the end of 2027.

Most Dutch entrepreneurs treat this like banking regulation. Something for financial institutions to handle.

Wrong.

The regulatory burden does fall on payment providers. But the operational consequences land on you.

Why the Transition Period is More Dangerous Than the Regulation

The danger is not the final state of PSD3. The danger is the 18 to 24 month transition period between now and late 2027.

How Silent Payment Failures Happen

Some payment providers will update their systems early. Others will wait. Your business sits in the middle, using multiple providers with inconsistent authentication flows, different hold periods, and altered dispute processes.

Inconsistency creates silent failures.

A customer completes checkout. The payment appears to process. But the new authentication step fails quietly in the background. No error message. No notification. Just a missing transaction that shows up three days later when your cash flow does not match your sales.

The iDEAL Migration Creates a Vulnerability Window

This is not theoretical. iDEAL is transitioning to Wero throughout 2026 and will disappear completely in 2027. iDEAL processes more than 1.5 billion transactions annually in the Netherlands. The payment method accounts for roughly 70% of online payments.

When a payment method this dominant undergoes a system migration, every business using it enters a vulnerability window.

Bottom line: The transition period creates process mismatches before the system stabilizes. These mismatches produce cash flow gaps you cannot immediately diagnose.

How PSD3 Changes Your Payment Operations

Expanded Fraud Liability Rules

PSD3 expands liability rules around fraud, particularly authorized push payment fraud. Payment providers must prove they applied Strong Customer Authentication correctly. If they did not, they carry the liability.

This sounds like protection for you. In practice, it means more verification steps for your customers.

More Verification Steps Lead to Payment Abandonment

More friction means more abandonment.

Research from 2019 showed that approximately one in three transactions are lost because of complex authentication flows. PSD3 enhanced security measures are designed to reduce fraud. During the adjustment period, they increase payment abandonment rates.

Your conversion rate drops. Not because your product changed. Because the payment system added steps.

Process Mismatches Create Cash Flow Dips

You also face extended hold periods. Altered chargeback routes. New rules around recurring payments and direct debits. These are not catastrophic changes. They are process mismatches. These mismatches create cash flow dips you cannot immediately diagnose.

What this means: Enhanced security protects consumers but creates merchant friction. The adjustment period produces temporary conversion losses and settlement delays.

Why Updated Terms of Service Transfer Risk to You

Your payment provider will send updated terms and conditions. Most founders will click accept without reading them.

Risk transfers to you at that moment.

What Updated Terms Redefine

The updated terms will redefine:

- Who owns liability when authentication fails

- How refunds and disputes are processed under the new rules

- What data you are required to provide for compliance

- How quickly funds settle after a transaction

Payment Systems Are Contractual Relationships

You need to know how these changes affect your refund approval process, your recurring billing logic, and your dispute handling. If you treat payment systems as passive utilities instead of contractual relationships, you lose visibility into where your cash flow vulnerabilities live.

Key point: Clicking accept without reading transfers operational risk from the provider to your business. Updated terms change settlement timing, liability allocation, and dispute resolution.

Three Controls to Install Before the Transition Period

You do not need to become a payments expert. You need to install three controls before the transition period creates problems.

1. Map Your Payment Provider Dependencies

List every payment method you accept. Identify which providers handle each one. Confirm whether they have communicated their PSD3 transition timeline. If they have not, ask.

2. Test Authentication Flows Before Customers Do

Run test transactions through your checkout process monthly during 2026 and 2027. Watch for new verification steps, error messages, or delays. Catch the friction before it costs you conversions.

3. Read the Updated Terms When They Arrive

Do not click accept reflexively. Read the sections on liability, dispute resolution, and settlement timing. If the language is unclear, ask your provider to explain it in operational terms. You need to know what happens when a payment fails, not what the legal clause says.

Action summary: These three controls give you visibility into payment system changes before they create cash flow gaps or conversion losses.

How Much PSD3 Compliance Preparation Costs

Small businesses will spend tens of thousands of euros on PSD3 compliance preparation through technology upgrades, staff training, and external consulting. Large organizations will spend millions.

You cannot avoid the transition. But you can avoid the silent failures from treating payment systems as something that works automatically.

The market does not break companies. Delay does.

Install the controls now. Map your dependencies. Test your flows. Read the terms.

Structure is cheaper than recovery.

Frequently Asked Questions About PSD3 for Dutch Businesses

When does PSD3 become mandatory for businesses in the Netherlands?

Full PSD3 compliance is expected by the end of 2027. The political agreement was reached in November 2025. The transition period runs from now through late 2027.

Do small businesses need to comply with PSD3 directly?

No. The regulatory burden falls on payment providers and financial institutions. Small businesses face operational consequences through changed authentication flows, settlement timing, and updated terms of service from their payment providers.

What happens to iDEAL under PSD3?

iDEAL is transitioning to Wero throughout 2026 and will disappear completely in 2027. iDEAL currently processes more than 1.5 billion transactions annually and accounts for roughly 70% of online payments in the Netherlands. This migration creates a vulnerability window for businesses relying on iDEAL.

How will PSD3 affect my payment conversion rates?

PSD3 requires stronger customer authentication. More verification steps create more friction. Research from 2019 showed approximately one in three transactions are lost because of complex authentication flows. During the adjustment period, conversion rates drop because payment systems add steps, not because products change.

What should I look for in updated payment provider terms?

Read sections on liability allocation when authentication fails, refund and dispute processing under new rules, data requirements for compliance, and fund settlement timing. Ask your provider to explain changes in operational terms, not legal language.

How often should I test my payment flows during the transition?

Run test transactions through your checkout process monthly during 2026 and 2027. Watch for new verification steps, error messages, or delays. Monthly testing catches friction before it costs conversions.

What are silent payment failures?

Silent payment failures occur when a customer completes checkout and the payment appears to process, but a new authentication step fails quietly in the background. No error message. No notification. The missing transaction shows up days later when cash flow does not match sales.

How much will PSD3 compliance preparation cost my business?

Small businesses will spend tens of thousands of euros on compliance preparation through technology upgrades, staff training, and external consulting. Large organizations will spend millions. You do not need to become a payments expert. Installing three controls before the transition period prevents expensive surprises.

Key Takeaways

- The transition period between now and late 2027 creates more operational risk than the final PSD3 regulation.

- Payment providers will update systems at different speeds. Inconsistent authentication flows produce silent transaction failures and cash flow mismatches.

- iDEAL disappears in 2027 as it transitions to Wero. This migration affects 70% of online payments in the Netherlands.

- Enhanced security adds verification steps. More friction increases payment abandonment rates during the adjustment period.

- Updated terms of service shift liability, refund processes, and settlement timing. Clicking accept without reading transfers risk to your business.

- Three controls prevent expensive surprises: map payment provider dependencies, test checkout flows monthly, and read updated terms carefully.

- Structure is cheaper than recovery. Install controls now before the transition period creates problems.