Late VAT filing destroys small businesses through cash flow mismanagement, not lack of knowledge. The core problem is treating collected VAT as business income instead of borrowed money. Since January 2025, Dutch penalties reach €5,514 maximum. Prevention requires separating VAT immediately, scheduling filing two weeks early, and tracking payment dates instead of invoice dates.

Quick Answer: How to Prevent VAT Cash Flow Problems

- Separate VAT into a different account the moment client payment arrives

- File two weeks before the deadline, not on the deadline

- Track when you receive payment, not when you send invoices

- Reconcile collected VAT against reported VAT monthly

- Remember: VAT is borrowed money held for the government, not your revenue

I’ve watched small service businesses collapse over VAT compliance.

The failure wasn’t sudden. It was a slow drift from “I’ll file next week” to “I can’t pay what I owe.”

Most Dutch entrepreneurs understand VAT basics. The problem isn’t knowledge. The problem is timing: when clients pay you versus when the tax office expects payment.

That gap creates a psychological trap.

LISTEN TO THE DEEP DIVE ABOUT THIS TOPIC:

How Does Late VAT Filing Start?

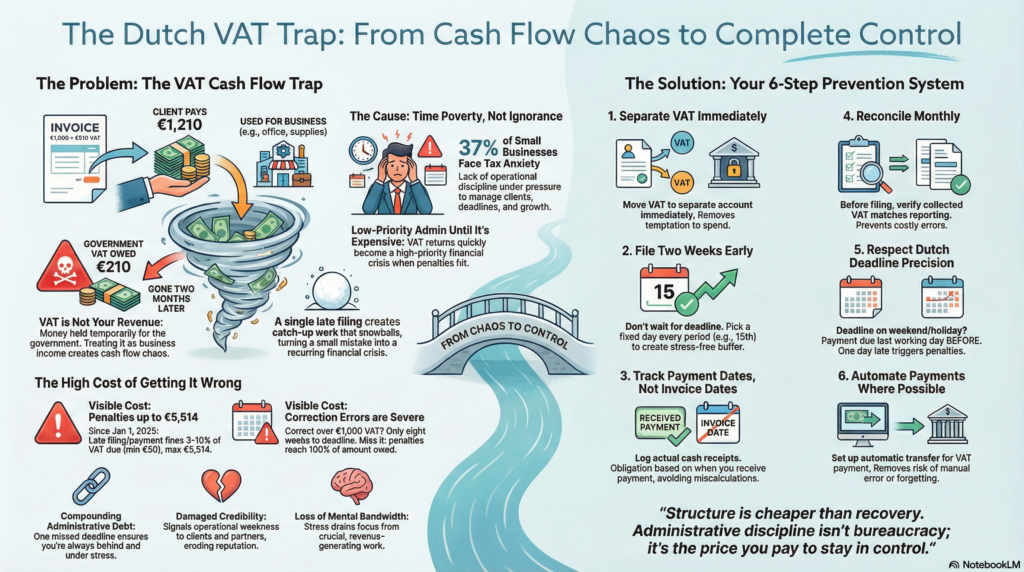

You invoice a client for €1,000 plus €210 VAT. The full €1,210 lands in your account. Your brain registers it as business income. You use it to cover expenses, salaries, or personal draws.

Two months later, the VAT return is due. You owe €210 you already spent.

This creates a cash flow gap you fill by delaying the filing. The delay becomes a pattern. The pattern becomes a crisis.

Bottom line: The psychological trap forms when you treat collected VAT as business income instead of borrowed government money.

Since January 1, 2025, the Dutch Tax Authorities increased penalties significantly. Late filing or payment can now trigger penalties up to €5,514 maximum, with charges between 3-10% of the VAT due (minimum €50).

If you discover you need to correct more than €1,000 in VAT, you have eight weeks to act. Miss that window and penalties can reach 100% of the amount.

The system doesn’t care about your intentions. It measures proof and timing.

Critical point: Penalties are based on proof and deadlines, not your financial situation or intentions.

Why Do Entrepreneurs Miss This Pattern?

The core issue is time poverty, not financial poverty.

Research shows that 37% of small businesses struggle with anxiety and confusion about tax filing. One-third don’t know if they need to pay estimated taxes. A quarter don’t know how to file at all.

Most of these entrepreneurs have college degrees. This isn’t about education. The gap is operational discipline under pressure.

When you’re managing client work, delivery deadlines, and business development, VAT returns feel like low-priority admin. They aren’t urgent until they’re expensive.

By then, you’re managing penalties instead of growth.

Core insight: Time poverty drives this problem, not financial poverty. VAT returns feel like low-priority admin work until they become high-priority financial crises.

What Are the Real Costs of Late VAT Filing?

The visible cost is financial penalties. The hidden cost is control.

Late VAT compliance creates these consequences:

Compounding administrative debt. One missed deadline triggers catch-up work that overlaps with the next filing period. You’re always behind.

Cash flow distortion. You treat VAT revenue as operating capital. When payment is due, you scramble to cover an obligation you thought you’d already handled.

Damaged credibility. Administrative patterns signal reliability. Clients and partners read late compliance as operational weakness.

Loss of mental bandwidth. The stress of knowing you’re behind drains focus from revenue-generating work.

The real damage isn’t the penalty amount. It’s the loss of control over your financial structure.

Key takeaway: Financial penalties are visible costs. Loss of control, mental bandwidth, and credibility are the hidden costs that destroy businesses.

What System Prevents VAT Cash Flow Problems?

You need fixed scheduling, not motivation.

Here’s the minimum system that keeps VAT manageable:

Separate VAT immediately. When client payment arrives, move the VAT portion to a separate account. Treat it as money you’re holding for the government, not business income. This removes the psychological trap.

Schedule filing on the same day every period. Don’t wait for the deadline. Pick a day two weeks before the due date and file then. This creates buffer time for corrections or payment delays.

Track payment dates, not invoice dates. Your VAT obligation is based on when you receive payment, not when you send the invoice. Log actual cash receipts to avoid miscalculating what you owe.

Install a pre-filing check. Before you file, verify that VAT collected matches what you’re reporting. One monthly reconciliation prevents expensive corrections later.

Mark Dutch deadline precision in your calendar. If a VAT deadline falls on a weekend or public holiday, payment must reach the Tax Authorities on the last working day before. Missing this by one day triggers penalties.

Set up automatic payment if possible. Remove the manual step. If you’ve calculated correctly, let the system handle the transfer on schedule.

These controls cost almost nothing to install. They prevent expensive recovery work.

Implementation note: This six-step system creates buffer time, prevents cash flow confusion, and removes manual failure points. Installation cost is near zero. Prevention value is enormous.

The Decision Rule

If you don’t have proof of when VAT was collected and when you paid it, you don’t have compliance. You have memory.

Administrative discipline isn’t bureaucracy. It’s the price of staying in control when pressure increases.

Structure is cheaper than recovery.

Frequently Asked Questions

What happens if I file my VAT return one day late in the Netherlands?

If the deadline falls on a weekend or holiday, payment must arrive on the last working day before. Missing by one day triggers penalties between €50 minimum and €5,514 maximum, plus 3-10% of the VAT due.

Should I treat VAT as business income?

No. VAT is borrowed money you hold for the Dutch Tax Authorities. Treating it as business income creates cash flow gaps when payment is due. Separate it immediately into a different account.

When is my VAT obligation triggered: invoice date or payment date?

Your VAT obligation is based on when you receive payment, not when you send the invoice. Track actual cash receipts to calculate what you owe accurately.

How much time do I have to correct a VAT mistake?

If you need to correct more than €1,000 in VAT, you have eight weeks to act. Miss that window and penalties reach up to 100% of the amount.

Why do small businesses struggle with VAT compliance despite understanding the basics?

37% of small businesses experience anxiety and confusion about tax filing. The gap isn’t education. It’s operational discipline under time pressure. VAT returns feel low-priority until they turn expensive.

What’s the minimum system to stay VAT compliant?

Separate VAT when payment arrives. File two weeks before the deadline. Track payment dates, not invoice dates. Reconcile monthly. Mark Dutch deadline precision in your calendar. Automate payment where possible.

How does one missed VAT deadline become a pattern?

One missed deadline triggers catch-up work that overlaps with the next filing period. You’re always behind. This creates compounding administrative debt and cash flow distortion that becomes a crisis.

What does late VAT filing signal to clients and partners?

Administrative patterns signal operational reliability. Late compliance reads as operational weakness. Credibility damage happens invisibly through these patterns.

Key Takeaways

- VAT is borrowed money held for the government, not business revenue. Treat it separately from the moment payment arrives.

- The mismatch between when clients pay and when VAT is due creates a psychological trap that leads to delayed filing and cash flow crises.

- Since January 2025, Dutch VAT penalties reach €5,514 maximum, with charges between 3-10% of VAT due (minimum €50). Corrections over €1,000 must happen within eight weeks or face 100% penalties.

- Time poverty drives late filing, not financial poverty or lack of knowledge. 37% of small businesses struggle with tax filing anxiety.

- Hidden costs include compounding administrative debt, damaged credibility, cash flow distortion, and loss of mental bandwidth.

- Prevention requires six controls: separate VAT immediately, file two weeks early, track payment dates instead of invoice dates, reconcile monthly, mark Dutch deadline precision, and automate payment.

- Structure is cheaper than recovery. Administrative discipline is the price of staying in control when pressure increases.