For owner-managers, tax risk starts when the contract route and the working route part company.

In a small group, a Dutch property lease can look calm. There is a lease, rent invoices, a BV name, maybe a STAK for the family shares. The founder sees order. Tax law may see control.

The signal has to become readable

The Gelderland judgment, ECLI:NL:RBGEL:2023:2738, shows the point in hard facts. The taxpayer and the partner privately owned the property and indirectly held all shares in A BV. Most of the property was leased to B BV. Adult children held the certificates in the structure, while the taxpayer and partner were STAK directors. One BV supplied catering and services to the other.

The lease is not the whole story

Article 3.92 Wet IB 2001 is built on a plain idea. If a taxpayer makes an asset available to a company in which the taxpayer or a connected person has an aanmerkelijk belang, the TBS rules can apply. The statutory wording reaches legal and factual, direct and indirect routes. It does not stop the analysis at the contract name.

In this case, B BV had no staff and was structurally loss-making. The court found that B BV had no independent economic meaning in the relevant facts. As a result, the property was treated as factually made available to A BV. For a small group, that is the lesson. A structure can be legally real and fiscally weak if the working reality points elsewhere.

Control leaves a trail

Dutch business life uses holdings and STAKs every day. KvK describes a holding BV as a parent company with one or more subsidiaries. It also explains that certification of shares can split voting rights and economic rights. That is normal. The danger starts when the structure carries more meaning than the facts can support.

What the signal changes

In a small company, control rarely hides well. It shows up in who has the keys, who signs contracts, who schedules staff, who speaks to customers, who carries losses, who sends invoices and who receives the benefit. It also shows up in board minutes, bank flows, rental pricing, service agreements and annual accounts. Those records should tell one story, not five.

Picture a family hospitality business. The parents own the building privately. One BV has the lease. Another BV has the staff, the catering activity and the customer value. The children hold certificates through a STAK, but the parents still steer the decisions. Years pass. Rent is booked. Parties are hosted. Invoices move between entities. Nothing feels unusual until a tax review reads the same facts as one pattern.

Cash follows the classification

TBS is not only a label. Belastingdienst guidance treats TBS income as box 1 income after deductible costs and the TBS exemption. That exemption is 12 percent of the TBS result. The taxpayer must keep an administration for the asset and prepare a balance sheet and profit and loss account.

For a DGA, that changes the conversation fast. Many founders think in holding terms: operating profit, salary, dividend and box 2. For 2026, Belastingdienst lists box 2 rates of 24.5 percent up to €68,843 and 31 percent above that amount. Box 1 goes to 49.50 percent above €78,426 for taxpayers aged 66 or younger. Historic years have their own rates, but the pressure point is obvious.

What founders should check

A made-available property can pull the result into box 1. It can also bring additional assessments, because Belastingdienst may issue a navorderingsaanslag when more tax is due than was previously assessed. For income tax, belastingrente is generally counted from 1 July after the tax year to one month after the assessment date. From 1 January 2026, the rate is 5 percent for all taxes except toeslagen and vennootschapsbelasting.

What a careful owner reads from this

The sensible reaction is not panic. It is a comparison between the contract route and the working route. A careful owner-manager can test whether a privately owned asset is used by any connected BV. The rent basis should make sense. The payment trail should be visible. If an intermediary company is meant to matter, it needs real substance, such as staff, risk, margin or decision-making.

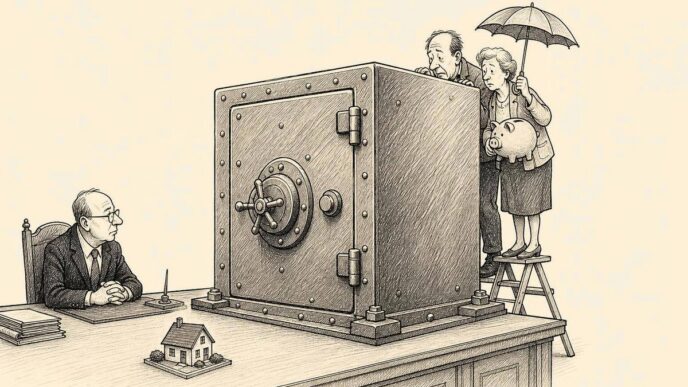

Where a STAK is involved, the governance file deserves the same care as the tax return. Who holds voting rights? Who receives economic rights? Who can change the operating route? Who decides when the business needs money, staff, renovation or a new lease? Those answers should be easy to read in the record.

The ledger then has to back the story. Rent invoices, intercompany agreements, service charges, valuation notes, board minutes and bank movements should fit together. They should not look like fragments from different deals. That is where micro and small companies are often exposed. Their structures grow in layers, while the family keeps making the decisions.

The quiet lesson

A property is often more than premises. It is collateral, family wealth, pension thinking, rental income and operating infrastructure at once. When the TBS rules reach it, the issue touches governance, valuation, cash, family control and the credibility of the company record.

Dutch tax does not stop at the company name on the invoice. Sometimes it follows the person who controls the route, the asset and the benefit. For a founder, that is not a reason to fear structures. It is a reason to make sure the structure and the business day tell the same story.

Sources

- A-G: pand via tussengeschoven bv toch feitelijk indirect tbs aan eigen ab-bv – Taxence

- Rechtspraak – A-G signal is not yet a final Supreme Court ruling

- Rechtspraak – Underlying TBS property dispute at first instance

- Wettenbank – Article 3.92 Wet IB 2001 legal basis

- Belastingdienst – Belastingdienst guidance on TBS assets

- Belastingdienst – Aanmerkelijk belang and box 2 comparison

- Belastingdienst – Current box 1 rate pressure

- Belastingdienst – Navordering and old-year exposure

Referenced in the article

Column | Ledger & Tax

Tax Plan 2027 Is Already Touching 2026 Cash Decisions

A two-cent travel allowance shows why founders should date assumptions before the law is final.

Column | Ledger & Tax

A Quiet Bond Can Still Move Your Box 3 Tax

Belastingdienst has made zero-coupon bonds a yearly value question, not a coupon question.

Column | Compliance

Old Dutch Tax Years Can Still Shape Tomorrow’s Cash

A short Hoge Raad ruling shows why dates, entity records and tax requests deserve quiet.

The Polder is written for readers who need the Dutch business environment translated into practical meaning. Corrections, source policy and editorial accountability are part of the publication record.