A finished year can still hide weak authority, broken software trails and slow tax answers.

Many Dutch founders know the relief of a closed year. VAT returns are filed. The accounts are prepared. The bank balance agrees with the statement. In a larger organisation, the audit opinion may even be clean.

The signal has to become readable

That feeling is natural. It is also incomplete. A finished year is not the same as a controlled company. The difference appears when someone asks for the route behind a number: a tax inspector, bank, subsidy desk, buyer, supplier, investor, payroll adviser or court.

The Comfort of a Finished Year

Amsterdam’s financial regulation, published on Overheid.nl, gives a sober definition that deserves attention outside city hall. It treats administration as the systematic collection, recording, processing and provision of information for steering, functioning, control and accountability. The business meaning is simple. Records are not a cupboard. They are the company’s memory under pressure.

The same regulation links administration to steering, control, insight into assets and liabilities, accountability and the control of registrations. Its rechtmatigheidsverantwoording uses a 2 percent threshold, while deviations above 0.3 percent must be explained in the bedrijfsvoering section with measures to prevent recurrence.

Under the Besluit accountantscontrole decentrale overheden, municipal audit opinions work with approval tolerances. For municipal accounts, the approval tolerance is 2 percent of the size basis, tied to total municipal costs excluding additions to reserves. It covers deviations in the financial statements and audit uncertainties. If that tolerance is exceeded, an unqualified opinion is not issued.

That is a useful signal for smaller businesses. A clean opinion, a closed year or a tidy annual report is not a certificate that every routine is healthy. It means the final picture passed a threshold. The daily route toward that picture may still be weak.

CBS gives the public scale. Dutch municipalities budgeted 84.6 billion euros in costs for 2026, 5.8 percent more than in the 2025 budgets. Social expenditure alone was budgeted at 36.3 billion euros, or 42.9 percent of municipal budgeted costs. At that size, tolerance is necessary. So is discipline.

What the signal changes

A small company has smaller numbers, but less room to absorb disorder. One duplicate supplier payment, one missing approval, one cancelled software subscription or one unexplained debtor balance can pull the owner away from selling, delivery and cash management.

Where Control Breaks First

Picture a small installation firm that changes its accounting and planning software. The new system looks better. Invoices are easier to send. A few months later, the owner cancels the old subscription because the migration seems complete.

Then a municipality asks for support on a subsidised project. The owner can show the invoice and the bank payment, but not the old approval trail, project allocation or source record behind the VAT treatment. Nothing dishonest happened. The weakness is different. The company cannot easily show the path from agreement to work, invoice, approval, payment, ledger and return.

That is where KVK’s guidance becomes practical. Basic administrative records must be kept for at least seven years. Records concerning immovable property and rights to immovable property must be kept for at least ten years. For digital records, the entrepreneur must keep access during the retention period to all used programs and stored information, including paid programs no longer in use.

A PDF export may help. It is not always enough. If the old data cannot be opened, searched, reconciled and connected to the new ledger, the company still carries the burden of the past without the tools to explain it.

Authority Is Part of the Evidence

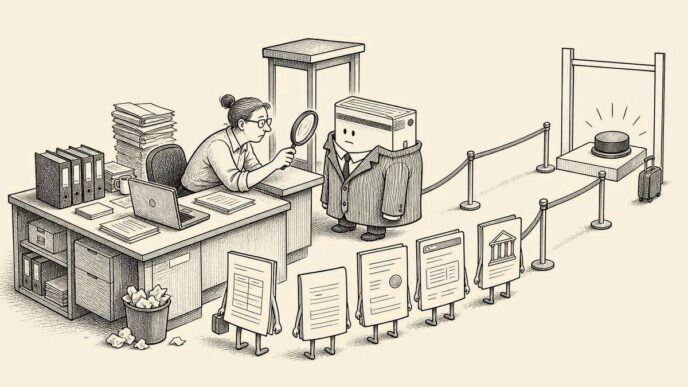

Control is often mistaken for bureaucracy. In a small business it is usually a set of plain questions. Who may approve spending? Who may change supplier bank details? Who reviews open items? Who can post journal entries? Who checks that old systems remain accessible? Who removes temporary rights after a system problem?

Amsterdam’s public system has separate council oversight through a Rekeningencommissie, with tasks around faithful and lawful financial management, financial organisation, control and risk management. A micro business does not need that architecture. It does need a miniature version of the same idea: maker, approver and reviewer should not blur without thought.

Digital access makes that sharper. Rijksoverheid reported that the Tweede Kamer adopted the Cyberbeveiligingswet and Wet weerbaarheid kritieke entiteiten bills on 15 April 2026. The Cyberbeveiligingswet implements the EU NIS2 directive. Once in force, organisations in scope face duties including duty of care, reporting and registration.

What founders should check

A company outside that legal scope can still learn from the direction of travel. Privileged access is not a convenience. It is a responsibility. Temporary administrator rights, emergency payment authority and manual corrections need a reason, a period, a reviewer and an end date.

Tax Turns Weak Records Into a Weaker Position

Belastingdienst gives the clearest SME anchor. Entrepreneurs are legally obliged to set up and maintain a good administration. Tax returns are based on that administration, and the tax authority must be able to check those returns quickly and properly.

If records are incomplete or not retained long enough, Belastingdienst may establish turnover and profit itself. If the entrepreneur disagrees, the entrepreneur must prove that the calculation is wrong. That is omkering van bewijslast. The practical issue is not only a possible correction. It is the loss of the normal position in the proof discussion.

This matters more when the market is already tight. CBS reported that Dutch entrepreneurial confidence fell to -14.8 at the start of the second quarter of 2026. Confidence was negative in all sectors, while more businesses expected selling prices to rise in the following three months.

When confidence is weak and prices are under pressure, poor records hurt faster. Debtor days become harder to read. Supplier balances carry old disputes. VAT figures are filed from accounts that technically close but do not explain themselves. Banks ask questions that take too long to answer. The cost is not only compliance risk. It is management attention.

The Owner’s Simple Test

A judgment published by Rechtspraak.nl on 26 May 2026, from the College van Beroep voor het bedrijfsleven, dealt with audit evidence after migration to a new IT environment. The case involved financial administration, invoice approval and project administration applications. The wider business lesson is plain enough: software output is not evidence by itself.

For many founders, the useful test is modest. Can the company follow a few sales invoices and purchase invoices from contract or order to invoice, approval, payment, ledger entry and tax treatment without reconstruction? Can it explain who had special system rights, why they had them and when those rights ended? Can it still open the old software that contains historic records?

Those questions do not require a thick manual. They require ownership. The founder, bookkeeper, adviser and key employee should know where the evidence lives and who is responsible for exceptions. A one-page map can often do more than a policy nobody reads.

Good administration is not the enemy of entrepreneurship. It is the memory that lets a business defend its own story. The mature company is not the one with the prettiest year-end folder. It is the one that can answer calmly when the question arrives.

Sources

- CBS source

- Accountant.nl

- Overheid.nl, Lokale wet- en regelgeving

- Overheid.nl, Lokale wet- en regelgeving

- Wettenbank

- CBS

- CBS

- Belastingdienst

Referenced in the article

Column | Market Pulse

Fewer Dutch Bankruptcies, but Payment Pressure Still Needs Attention

April's CBS figures show fewer court failures. Closures, cautious consumers and sector stress still leave.

The Polder is written for readers who need the Dutch business environment translated into practical meaning. Corrections, source policy and editorial accountability are part of the publication record.