For non-EU entrepreneurs, the Dutch refund route is moving from forms to portal discipline.

A British design studio comes to Utrecht for a trade fair. It pays Dutch VAT on stand construction, local transport, hotel rooms, printing, equipment hire, and a few supplier invoices that looked routine while the team was racing toward opening morning. Back home, the owner books a refund receivable and treats it as money on the way.

The signal has to become readable

That is where the real shift begins. The VAT may still be recoverable. From the second quarter of 2026, companies based outside the EU that do not file Dutch VAT returns in the Netherlands must use Mijn Belastingdienst Zakelijk. Paper applications will no longer be possible. Communication will run through the portal.

Access comes before entitlement

The practical change is simple enough to say and easy to mishandle. The first question is no longer only whether the invoice carries Dutch VAT. The first question is whether the company can enter the Dutch system, has the right registration, can prove business use, and knows which deadline is actually running.

Belastingdienst requires a valid login method, DigiD or eHerkenning depending on the legal form. Without that login, the application cannot be submitted. Email notifications will tell the business when documents or actions are waiting in the portal. Someone has to watch the channel, not just prepare the tax calculation.

The refund window starts early

For non-EU entrepreneurs in this route, the refund claim must be submitted before 1 July of the following year. The official form describes the timing as within six months after the end of the calendar year for which the refund is requested. That sounds neat until June arrives and the company still lacks a Dutch registration number or cannot get into the portal.

This is a timing problem as much as a tax problem. A disputed invoice can be reviewed. A missing login can stop the claim before anyone reads the invoice. For a small foreign company, that difference matters to cash flow, especially when the refund was already built into the forecast.

Route choice decides the cash

The line between the refund application route and the Dutch VAT return route is not cosmetic. A non-EU company that does not file Dutch VAT returns may belong in the refund route. A foreign entrepreneur with a Dutch VAT return obligation follows another route, with digital VAT returns generally due within two months after the end of the period. That two-month clock also applies when there was no Dutch activity and when a refund is due.

What the signal changes

So the first control question is route selection. Non-EU status alone does not settle it. Seat of business, fixed establishment, Dutch taxable supplies, and reverse-charge situations can all matter under Dutch VAT law. A company can lose time by preparing the right numbers for the wrong door.

For the owner in the Utrecht fair example, this is not theory. If the refund sits in the cash forecast for autumn, the route decides whether that forecast is serious. A VAT receivable in the ledger is not the same as cash that will arrive on time.

The invoice still needs a story

The Dutch rules keep the substance test in place. The goods or services must be used for the business and for activities over which VAT is charged. The VAT must have been charged to the entrepreneur, and it must be VAT that would be deductible as input tax for a Dutch entrepreneur. Foreign status does not repair a weak cost.

That matters for ordinary spending. VAT on food and drink in catering establishments can never be deducted. VAT on overnight accommodation and similar costs may be deductible when linked to taxed services. If costs support both taxable and exempt activities, the input VAT has to be split.

A court signal on housing

The point becomes clearer in court. In April 2026, Rechtbank Zeeland-West-Brabant denied a Polish company a Dutch VAT refund on employee housing. The company supplied personnel in the Netherlands, but the court found that it had not made plausible that employees had no real choice in accepting the housing, and had not shown special business circumstances forcing the accommodation.

That case was not about the non-EU portal change. Still, it carries the same practical lesson. An invoice is evidence, not a conclusion. The business facts must support the VAT treatment.

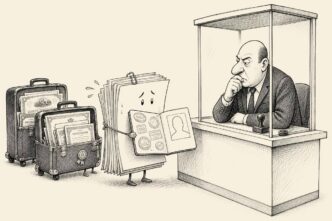

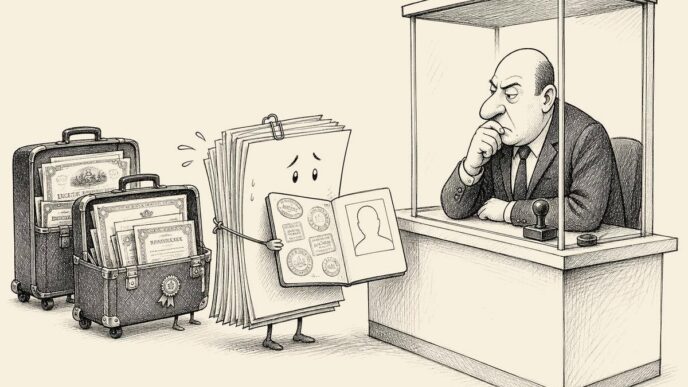

Registration is part of the tax position

A non-EU refund applicant needs a Dutch registration number. The registration process can ask for proof of activity, foreign registration proof where relevant, a non-EU tax statement, identity or incorporation documents, representative authorisation, and translations if documents are not in Dutch, German, or English.

What founders should check

This is where small companies often underestimate the work. The accountant may know the refund rule. The founder may know the cost was business-related. The adviser may even have the invoices. But if the registration pack is incomplete, or the portal mandate is unclear, the refund is not yet operational cash.

The wider Dutch VAT system is also being modernised. State Secretary Eerenberg informed the Tweede Kamer about that modernisation on 17 March 2026. The non-EU refund move sits inside that broader rebuild. System changes tend to expose old habits: shared inboxes, informal adviser access, scattered receipts, and invoice folders that cannot explain the business reason for a cost.

A calm habit before the claim

For the British studio, the better habit starts before the next Dutch event. The company can separate Dutch VAT costs by period, supplier, VAT amount, cost type, and business use. It can mark catering VAT away from recoverable VAT. It can keep hotel and travel costs tied to the taxable project. It can confirm whether it belongs in the refund route or the VAT return route before the deadline becomes uncomfortable.

Expected refunds should stay conditional liquidity until access, registration, evidence, and timing are ready. That is not pessimism. It is honest cash discipline. A small company should not let a receivable flatter the margin if the route to recovery is still unfinished.

The Dutch refund system is becoming less forgiving of loose administration, but not more mysterious. The practical standard is clear enough. Know the route. Secure access. Keep the evidence close to the ledger. Make sure one person owns the portal notifications, with a backup when that person is away.

The VAT refund is still about tax entitlement. From 2026, it is also about whether the business can prove, submit, and respond through the Dutch system. For small foreign entrepreneurs, that is the real change. Recoverable VAT is not automatic working capital. It becomes cash only when the route and the record are ready together.

Sources

- PwC Nederland

- Belastingdienst

- Belastingdienst

- Belastingdienst

- Belastingdienst

- Wettenbank

- Belastingdienst

- Belastingdienst

Referenced in the article

Column | Compliance

AI Makes Audit Judgement Faster, and Evidence More Exposed

The useful question for small firms is not whether AI helps, but whether the trail.

Column | Ledger & Tax

A Box 3 Fund Needs Real Rights, Not Just Paper

A Court of Appeal ruling shows why transfer rights, registers and tax-year records.

The Polder is written for readers who need the Dutch business environment translated into practical meaning. Corrections, source policy and editorial accountability are part of the publication record.