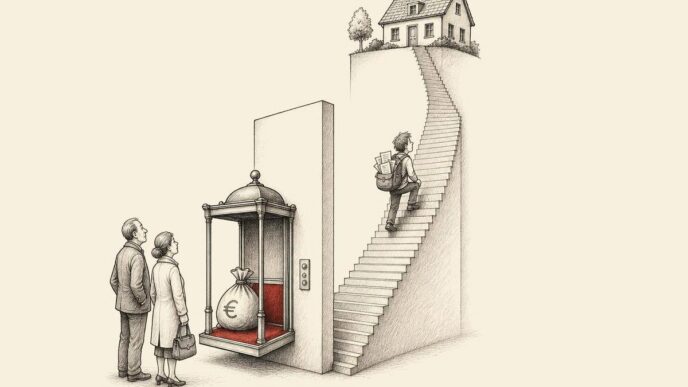

A second purchase before completion can turn a low-rate assumption into a cash-flow problem.

Dutch transfer tax follows the delivery moment, not the emotional order of the housing search. For a normal home transfer, the notarial deed is decisive. What the buyer declares there must fit the facts already visible on that day.

The economic route comes first

That is the practical lesson in a Court of Appeal judgment from Gerechtshof 's-Hertogenbosch, decided on 6 May 2026 and published by Rechtspraak on 26 May. The taxpayer and her partner bought a first home on 31 January 2021. Before that home was delivered on 1 July 2021, they signed a purchase agreement for a second home on 28 June. The 2% transfer-tax rate was applied at delivery of the first home. The tax inspector later reassessed the transaction at the 2021 8% rate.

What the court saw

The later sequence mattered. The first home was put up for sale on 31 July 2021, sold on 25 August, and the taxpayers moved to the second home around 27 October. The court held that, at the acquisition moment, the taxpayer had not made it plausible that she still intended to use that home otherwise than temporarily as her main residence. A better home, proximity to family and work, and uncertainty about financing or zoning for the second home did not change that reading.

This judgment reads less as a niche tax case and more as a clean warning about timing. In Dutch real estate, sincerity is not enough. The declaration has to survive the dated transaction record.

The notary date does real work

Under the 2026 statutory structure, the transfer-tax map is clear. Article 14 of the Dutch Legal Transactions Tax Act sets a 2% rate for a natural person who acquires a home and will use it otherwise than temporarily as the main residence, with the required declaration. Homes outside that route sit at 8%. Other immovable property falls under the general 10.4% rate.

The declaration is not ceremonial. Belastingdienst guidance says the signed declaration must be with the notary before transfer. When a notarial deed is used, the notary files and pays the transfer-tax return on the buyer's behalf. That makes the process feel handled. It does not erase the buyer's factual position.

Legal form is not the whole story

Take a small, realistic example. A freelance architect signs for a house in February because it fits the family budget and the school run. In June, before delivery, another house appears closer to a major client and to grandparents who help with childcare. The second agreement is signed, with financing still pending. At the first delivery, the low-rate declaration may still feel natural because the original plan once existed. The sharper question is simple: what did the facts say on the day ownership passed?

A second home can change the cash picture

Many micro-entrepreneurs keep the family home separate from the company. On paper, that can be correct. In cash terms, the wall is often thinner.

A ZZP worker, founder or DGA may use private reserves to support the business, keep a tax buffer, cover a slow payment month, or protect payroll timing. A private reassessment can land in the same bank reality as business pressure.

The market makes this more relevant. CBS reported that existing owner-occupied homes were 4.3% more expensive in April 2026 than one year earlier, with 19,454 housing transactions recorded by Kadaster that month. CBS also reported 75,403 homes sold in the first four months of 2026, more than 7% more than one year earlier. Kadaster said more than 76,000 homes were sold in Q1 2026, 18% more than a year earlier, and about 1,700 second homes were sold while about 300 were bought.

Those figures do not change the tax rule. They explain the pressure around it. In an active and expensive market, buyers overlap decisions. They keep searching after signing. They accept conditions. They move quickly when a better opportunity appears. That behaviour is understandable. It still needs a tax timeline that can carry its own weight.

Follow one revenue stream

The cash difference is not small. CBS reported an average transaction price of €486,101 for an existing owner-occupied home in April 2026. At 2%, transfer tax on that amount is about €9,722. At 8%, it is about €38,888. The difference is about €29,166 before tax interest, professional costs or financing effects. For a small business owner, that can equal a payroll buffer, several months of private drawings, a VAT reserve, or a postponed investment.

The timeline should be honest before the deed

The practical discipline is simple, but it has to happen early. Before delivery, the buyer's housing timeline should already be readable: purchase agreements, financing conditions, notarial dates, listing instructions, sale dates, intended occupation, actual moving plans, and any second purchase. If another home has already been bought before delivery, the 2% position deserves careful review before the deed is signed.

Each acquirer also has a separate position. Partners may buy together, but the declaration route still asks whether each buyer meets the conditions. The starters exemption is a separate regime, with its own 2026 conditions, including the 18 to 35 age range and the €555,000 value cap. The same hinge returns there as well: acquisition moment, main-residence use, and a declaration that matches the facts.

The larger lesson is professional hygiene. Do not let the notarial appointment become the first moment when the tax story is tested. By then, the facts may already be pointing somewhere else. A lower rate should be budgeted as a position that must be supported, not as a comfort attached to the first version of the housing plan.

Dutch real estate often rewards speed, especially when supply is tight and family needs are moving. Dutch tax administration rewards something different: dated consistency. The two can live together, but only if the buyer treats timing as part of the transaction, not as a memory to reconstruct after completion.

A second home bought too early does not make anyone careless. It does make the first home's tax story harder. Before delivery, the question is not only where you hope to live. It is whether the record on that day can honestly say the same thing.

Sources

Referenced in the article

Column | Ledger & Tax

A Faster BPM Portal Still Needs the Right Hands on It

Dutch vehicle tax is moving online, but registration still depends on identity, mandate and payment.

Column | Ledger & Tax

The Lorry-Charge Discount Will Not Fix a Weak Road-Cost Ledger

A temporary Dutch rate cut gives transport-heavy firms breathing room, but July still asks a sharper.

Column | Human Resources

When Sickness Files Become the Gatekeeper for Dutch Employers

A sickness file now shapes payment timing, privacy and reintegration for own-risk.

The Polder is written for readers who need the Dutch business environment translated into practical meaning. Corrections, source policy and editorial accountability are part of the publication record.