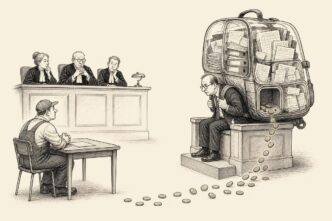

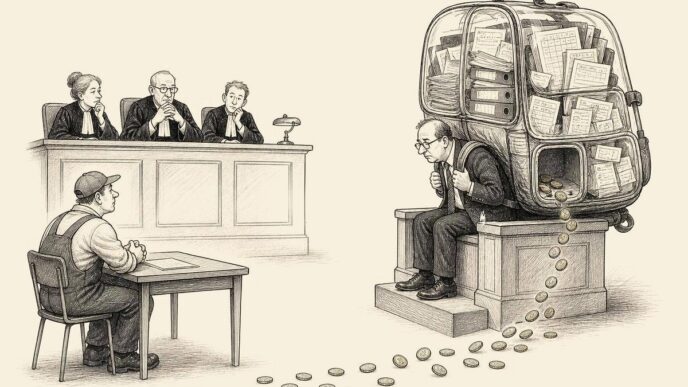

Customs representation can decide who faces duty, VAT pressure and recourse when an import is corrected.

An import declaration can look like a technical moment. Goods arrive, a declaration is lodged, a release follows, the lorry moves, the customer waits. In that rhythm, representation can feel like a setting in the system.

The signal has to become readable

I see it differently. In Dutch import practice, customs representation is one of the quiet places where authority, tax exposure, cash and recovery meet. It decides who stands before customs, who may be treated as debtor, who has to produce the documents, and who may later discover that a commercial promise is weaker than the legal position on the declaration.

This is not a concern for large logistics groups alone. CBS reported provisional Dutch goods imports of 581.9 billion euro in 2025 and exports of 654.8 billion euro. Both flows grew by 1.4 percent compared with 2024. Small importers, web shops, wholesalers, repair businesses and niche manufacturers all move inside the same control environment. The scale is macro. The mistake is often small.

The declaration is not just a form

Under the Union Customs Code, the basic frame is clear. The declarant is the person lodging a customs declaration in their own name, or the person in whose name the declaration is lodged. A customs representative may act directly, in the name of and on behalf of another person, or indirectly, in their own name but on behalf of another person.

That distinction matters because customs debt follows legal position. For release for free circulation, the customs debt is incurred when the declaration is accepted. The declarant is the debtor. In indirect representation, the person on whose behalf the declaration is made is also a debtor.

A representative must state that they act for another person and specify whether the representation is direct or indirect. If someone states representation without authority, the Union Customs Code treats that person as acting in their own name and on their own behalf. Customs authorities may ask for evidence of that authority.

This is where routine becomes risk. The declaration field, the mandate, the shipment instruction, the commercial contract and the VAT treatment need to tell the same story. If they do not, the discussion after a correction may no longer be only about value, classification or origin. It may become a discussion about who legally imported the goods.

A small scenario with a large consequence

Imagine a Dutch logistics provider clears goods for a foreign seller. A standard power of attorney is on hand. The goods are released, sold onward and paid for. Months later, a correction follows. Perhaps the customs value changes. Perhaps a classification point increases duty. Perhaps the goods fall into a more sensitive regulatory category.

What the signal changes

At that point, everyone reaches for the same assumption: the foreign seller was the real importer, the logistics provider only helped. Customs law does not work on assumptions. It asks who lodged the declaration, in what capacity, on whose behalf, and with what authority. If direct representation was not validly supported, the person who acted may carry a different exposure than expected.

Dutch case law has already shown how sharp that can be. In a 2018 Hoge Raad customs case, the issue included direct representation and customs debtor status. The published judgment records that the power of attorney was not legally valid, that no attributable appearance of authority existed, and that the represented company was not treated as customs debtor. The lesson is simple enough for daily practice: a label in the declaration does not repair a weak mandate.

A 2020 Rechtbank Noord-Holland case adds a more operational point. In that import dispute, the court considered that a sufficient and complete power of attorney for a particular import shipment required a specific clearance instruction. The specific instruction was missing, and the claimant had not acted as direct representative. That does not turn every general mandate into a failed mandate. It does show why the shipment link can matter.

The VAT and CBAM layers make the question heavier

Customs representation is often discussed as if it concerns duties only. In the Netherlands, that is too narrow. Import VAT, Article 23 treatment and fiscal representation can sit in the same commercial arrangement, while remaining legally different from customs representation.

The Belastingdienst explains that Article 23 allows import VAT, with a permit, to be reported through the VAT return instead of being paid immediately at import. Foreign entrepreneurs cannot apply for an Article 23 permit themselves. They may use a fiscal representative, and with a limited fiscal representative they may use that representative’s Article 23 permit in certain cases.

That is useful for cash flow, but it also creates a control question. The customs representative, the fiscal representative, the importer for VAT purposes and the commercial risk bearer are not automatically the same person. If a small business uses a forwarder, a fiscal representative and a foreign supplier in one chain, the administration has to show which role belongs to whom.

CBAM makes this more visible from 2026. Dutch Customs explains that the transitional phase for the Carbon Border Adjustment Mechanism ran until 31 December 2025 and that full application starts on 1 January 2026. For CBAM goods, such as certain steel, aluminium and fertilisers, importers must be admitted as authorised CBAM declarants. With direct representation, the importer remains responsible for CBAM obligations. With indirect representation, the parties must agree who acts as importer under the CBAM regulation.

What founders should check

That is a clear signal. Representation is no longer only a debtor question after an import correction. For some goods, it also connects to admission, reporting and certificate obligations.

The control trail is part of the position

Dutch Customs’ DMS document process points in the same direction. Documents for DMS import and export declarations have to be sent in a structured way, with separate emails, declaration numbers, selection messages and attachment requirements. Customs may still ask for original documents, and certain documents may have to be brought to the customs office within a set period.

This sounds procedural, but it has a practical meaning. The import position is not proven by one document alone. It is proven by the trail: the declaration, the mandate, the authority of the signatory, the shipment instruction, the invoice, the transport documents and the VAT handling. Where relevant, the CBAM position belongs in the same file. The commercial agreement on recovery belongs there too.

I would not treat this as paperwork discipline for its own sake. The real question is whether the company knows who it allowed to stand in front of customs. If an import correction arrives, the answer must already be visible. Searching for authority after the event is always weaker than having the role clear when the declaration was accepted.

For a micro or small business, this does not require drama. It asks for a sober habit. When a forwarder says it acts directly, the business needs to know who granted that authority and whether the person could grant it. When indirect representation is used, the business needs to understand that debtor exposure may be shared. When Article 23 or fiscal representation is involved, the VAT position should not be confused with the customs position. When CBAM goods are involved, the importer role deserves separate attention.

The commercial contract also matters. If customs addresses one party, but the cost belongs commercially to another, recovery depends on more than goodwill. It depends on whether the contract, instruction and documents make that recovery realistic. A weak recovery clause after a strong customs demand is a painful combination.

The calm conclusion is also the sharp one. Customs representation is not an administrative decoration on the import process. It is a legal and fiscal position with cash consequences. The business that can connect authority, declaration, VAT treatment, regulatory duty and recovery has not only tidied its documents. It has reduced the chance that a correction turns into a dispute about identity.

Sources

- CBS source

- EUR-Lex

- Belastingdienst Douane

- Belastingdienst Douane

- Belastingdienst Douane

- Belastingdienst

- Belastingdienst

- Rechtspraak

Referenced in the article

Column | Governance

High Dutch WOZ Values Ask for Evidence, Not Outrage

The housing market feels stretched, but a small owner wins a valuation argument with object data, not.

Column | Human Resources

Dutch Flex Work Is Becoming a Ledger Question

The 2028 proposal does not end flexibility. It makes availability visible in contracts, rosters and cash.

The Polder is written for readers who need the Dutch business environment translated into practical meaning. Corrections, source policy and editorial accountability are part of the publication record.